The Near Future Alongside Electric Air Transportation

Continue readingThe Near Future Alongside Electric Air Transportation

Continue reading

Jamie Dimon’s Recent Thoughts on AI and the Economy

Continue reading

Markets took a break from recent highs as investors relaxed ahead of this week’s key inflation data and corporate earnings.

Continue reading

Instilling good financial habits in children has become more crucial than ever. One of the key skills that can pave the way for a successful and secure future is learning how to save money. In this comprehensive guide, we will delve into the essential aspects of ‘how to save money as a kid,’ exploring the best ways to foster a sense of financial responsibility and independence from a young age.

Imagine the first dollar saved by a child as the cornerstone of a financial fortress. As kids navigate adulthood, this foundation becomes their unwavering support, providing financial security when facing responsibilities such as funding education, purchasing a home, or overcoming unexpected challenges. The seeds planted in childhood evolve into a shield that guards against life’s uncertainties.

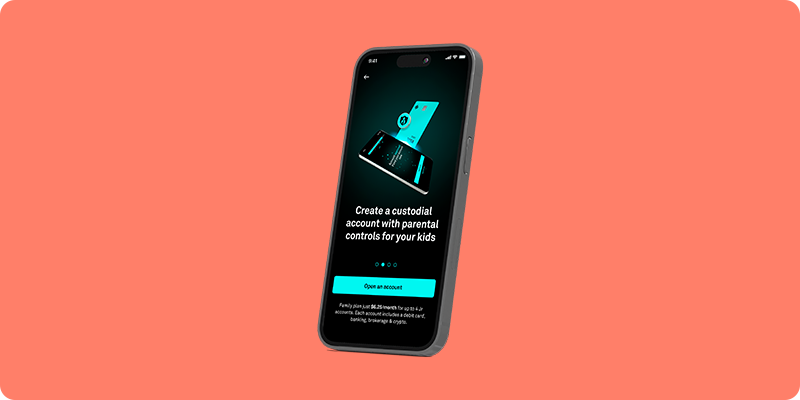

Understanding the significance of financial literacy, especially for the younger generation, lays the foundation for a lifetime of wise money management. As parents and guardians, guiding children toward the best way to save money for kids can empower them to make informed decisions about their finances in the future. One effective tool in this journey is Invstr Jr, a custodial account designed to cultivate financial knowledge and responsibility in children.

Educational opportunities blossom as savings accumulated during childhood open doors to a world of possibilities. Whether it’s financing college tuition or enrolling in specialized courses, the commitment to financial prudence becomes a tangible manifestation of the early dedication to economic empowerment. Teaching kids the importance of setting aside funds for emergencies instills resilience and adaptability. The financial safety net woven in childhood serves as a beacon in uncertain times, offering a lifeline when unexpected challenges arise.

As kids mature into adults, the significance of financial independence takes center stage. The early lessons of saving evolve into a roadmap for navigating the complex terrain of financial autonomy. The child who once saved diligently now stands on the precipice of financial independence, empowered to make informed decisions and carve their path. Teaching kids to spend less than what they make is a lifelong financial philosophy. The importance of saving money as a kid goes beyond childhood; it lays the foundation for a lifetime of financial success and independence. The lessons learned, from turning saving into a habit to spending less than what you make, become guiding principles that shape responsible financial behavior throughout adulthood. As kids embark on the journey of financial literacy, they carry with them not just practical skills but a mindset that empowers them to navigate the complexities of the financial world with confidence and competence.

Now, let’s explore the key strategies and practices that can help kids develop a robust savings mindset. From setting realistic savings goals to embracing the concept of delayed gratification, this article aims to be a comprehensive resource for parents, educators, and young minds eager to learn about financial wellness. Join us as we unravel the secrets of how to save money for kids and discover the transformative impact it can have on their financial future.

In the intricate tapestry of a child’s life, the significance of learning how to save money weaves threads of financial responsibility, independence, and future security. While it might seem like a small step, the impact of instilling a savings mindset from a young age can reverberate throughout their entire lives. Let’s delve deeper into why saving money as a kid is so crucial and then explore practical methods that can help kids save more effectively.

The importance of saving money as a kid extends beyond the immediate benefits. Fostering a habit of saving early on equips children with fundamental financial skills that can shape their future. Here are some key reasons why it matters:

Saving from an early age establishes a foundation for financial security. As kids grow older, they may face various financial responsibilities, such as education, buying a car, or even starting a business. A well-established savings habit equips them to handle these expenses responsibly.

Whether it’s saving for college or vocational training, having a savings fund can open doors to educational opportunities. This early financial preparation empowers kids to pursue their dreams without the burden of excessive student loans.

Life is unpredictable, and having savings provides a safety net during unexpected situations. Teaching kids to save for emergencies instills resilience and the ability to navigate unforeseen challenges.

Understanding the value of money and how to manage it responsibly contributes to the development of financial independence. Kids who grasp the concept of saving are more likely to make informed financial decisions as adults.

Now that we’ve established the importance of saving money as a kid, let’s explore practical methods that children can employ to maximize their savings.

Turning saving into a habit is the first step towards financial empowerment. Rather than viewing it as a one-time task, encourage kids to make saving a regular practice. This can be achieved by setting aside a fixed percentage of any money they receive. For example, if a child receives a $10 allowance, allocating $2 to savings becomes a routine that gradually builds wealth over time.

Encourage kids to create a “savings ritual,” whether it’s putting money into a piggy bank every Sunday or using a dedicated savings jar. This not only makes the act of saving more tangible but also instills the notion that saving is an ongoing process, not just a one-time event.

Kids thrive on goals, and setting specific saving goals can provide a sense of purpose and motivation. Help them identify what they want to achieve, whether it’s purchasing a favorite toy, saving for a trip, or even contributing to a charity. Creating a visual representation of their goals, such as a savings chart or jar, transforms the abstract idea of saving into a tangible, achievable target.

For example, if a child aims to buy a $50 video game, break down the goal into manageable steps. If they receive a $5 weekly allowance, show them that saving $2 each week will accumulate to $50 in approximately five months. This not only teaches patience but also illustrates the power of consistent savings toward a specific objective.

Budgeting is an essential aspect of effective money management. Introduce the concept of budgeting to kids by helping them categorize their income into different sections: savings, spending, and sharing. By understanding the allocation of funds, kids develop a conscious awareness of where their money goes, laying the groundwork for responsible financial behavior.

Start by creating a simple budget together. Use three jars or envelopes labeled “Save,” “Spend,” and “Share.” When the child receives money, guide them to allocate a percentage to each category. For example, if they receive $10, they might decide to save $3, spend $5, and set aside $2 for sharing or charitable contributions.

Creating a saving plan involves breaking down larger goals into actionable steps. Guide kids in outlining the specific actions they need to take to achieve their savings objectives. For instance, if they aim to save $50 for a new video game, the plan might involve saving $5 per week. This strategic approach not only teaches planning but also imparts the importance of perseverance in reaching financial milestones.

Sit down with the child to create a saving plan for their chosen goal. Use a calendar or planner to mark milestones and celebrate achievements along the way. If they encounter challenges, discuss adjustments to the plan, reinforcing the idea that flexibility is a crucial aspect of financial planning.

Introduce the concept of a child-friendly savings bank account as a secure haven for their money. Platforms like Invstr Jr offer not only a safe space for savings but also an educational tool to foster financial awareness. Walk them through the process of depositing money, checking balances, and understanding how interest works. This practical experience instills a sense of responsibility for their financial resources.

Take a field trip to a local bank or credit union to open a savings account for the child. Explain the concept of interest as a reward for saving money. Platforms like Invstr Jr also provide a digital experience, allowing kids to track their savings and investments online. Encourage them to set savings goals within the platform, creating a seamless integration of technology into their financial education.

An allowance serves as a child’s first introduction to earning income. Connect the dots between effort and reward by encouraging the completion of age-appropriate chores in exchange for an allowance. This not only instills a strong work ethic but also provides a consistent source of income for saving. Emphasize the importance of regular effort and responsibility in maintaining a steady financial inflow.

Work with the child to establish a chore chart that aligns with their capabilities. Assign a specific monetary value to each chore, and let them see the direct correlation between their efforts and the income they earn. Consider incorporating a bonus system for consistently completing tasks, reinforcing the idea that dedication and hard work are rewarded in the financial realm.

For older kids, exploring part-time jobs or odd jobs within the community can significantly accelerate their savings. Whether it’s babysitting, lawn mowing, or helping neighbors with tasks, these opportunities not only supplement income but also impart valuable life skills. Kids learn the importance of time management, responsibility, and interpersonal communication while earning extra money to bolster their savings.

Guide older kids in assessing their skills and interests to identify potential part-time or odd job opportunities. Discuss the importance of balancing work commitments with school and other responsibilities. Encourage them to create a simple resume or flyer highlighting their services, teaching them the basics of marketing themselves within the community.

Teaching kids to spend less than what they make is a fundamental principle of financial management. Help them understand the difference between needs and wants, emphasizing the importance of mindful spending. Practical examples, such as packing lunch instead of buying, or choosing generic brands over expensive ones, demonstrate the impact of small, conscious choices on overall savings. This principle ensures that their savings grow steadily, creating a solid financial foundation.

In the realm of financial education, saving money as a child unfolds as a journey shaping a lifetime. Early savings lay the groundwork for a robust financial fortress, providing security amidst life’s unpredictabilities. Practical methods, like fostering saving habits and embracing child-friendly savings accounts, form crucial elements in this financial narrative. As children transition to adulthood, earning allowances and engaging in part-time jobs become the stepping stones to a fulfilling career. The commitment to spend less than one earns evolves into a lifelong financial philosophy, ensuring a prosperous financial future. Saving as a child resonates as an enduring anthem of empowerment and financial competence.

All investing involves risk and can lead to losses.

Past performance does not guarantee future results.

Invstr Financial LLC (Invstr) is registered as an advisor with the SEC. Securities trading is offered to self-directed investors by Social Invstr LLC, a member of FINRA.

Markets started lower as investors continued to follow corporate earnings after the extended weekend.

Continue reading

The earnings report by the largest company by revenue.

Continue reading

The advanced merger talks between Capital One and Discover.

Continue reading

In the dynamic landscape of today’s economy, the need for financial literacy among teenagers is more crucial than ever. As adolescents stand on the brink of adulthood, the ability to navigate personal finances becomes an indispensable life skill. This article, Financial Literacy for Teens: Essential Financial Tips for Teenagers, is a compass for both teens and parents, guiding them through the nuances of managing money wisely.

Recognizing the pivotal role financial literacy plays in shaping a secure future, our focus is to provide actionable insights tailored specifically for teenagers. From budgeting basics to the principles of responsible spending, this guide aims to empower young minds with the knowledge needed for sound financial decision-making.

Embedded seamlessly within the fabric of our discussion are practical solutions to foster financial awareness. One such innovative tool is Invstr Jr, a custodial account designed to introduce teens to the world of investing. Throughout this article, we will naturally weave in tips on personal finance for teens, ensuring that the journey toward financial literacy is both informative and engaging.

As we explore the essentials of financial management for teenagers, our goal is to support the younger generation and their parents on this educational journey. Stay tuned for expert advice and valuable tips, with a subtle spotlight on Invstr Jr as a powerful resource in cultivating a robust financial foundation for the next generation.

Financial literacy lessons for teenagers

One primary reason for prioritizing financial literacy for teenagers is the transitional phase they find themselves in. As they inch closer to independence, teenagers are increasingly exposed to a myriad of financial scenarios – from managing an allowance to making informed choices about higher education expenses. Without a foundational understanding of personal finance, these challenges can quickly become overwhelming.

Parents, guardians, and adults play a pivotal role in providing the necessary guidance during this transformative period. By instilling financial literacy in teenagers, we equip them with the tools to navigate the complexities of budgeting, saving, and investing. This, in turn, fosters a sense of responsibility and confidence in handling financial matters.

Furthermore, the modern world presents teenagers with a plethora of financial choices, ranging from opening their first bank account to making decisions about student loans. Without a grasp of financial literacy, they may find themselves susceptible to pitfalls such as debt accumulation and poor spending habits. Teaching them the principles of budgeting, the importance of saving, and the potential benefits of investing arms them with the knowledge needed to make sound financial choices.

Moreover, financial literacy serves as a safeguard against the allure of instant gratification. In a society driven by consumerism, teenagers often face the temptation to succumb to impulsive spending. Educating them about smart spending, delayed gratification, and the value of long-term financial goals fosters a mindset that is essential for building a secure financial future.

In essence, the importance of financial literacy for teenagers lies in its ability to provide them with a solid foundation for the challenges that lie ahead. By investing time and effort in their financial education, parents and guardians contribute significantly to the development of a generation capable of making informed and responsible financial decisions, ultimately preparing them for a successful and secure future.

13 Top tips in financial literacy for teenagers

As teenagers embark on their journey towards financial independence, acquiring essential financial literacy skills becomes paramount. Here are 13 top tips to guide teenagers in shaping a solid foundation for a secure financial future:

Understanding the distinction between needs and wants is fundamental. Needs are essentials like food, shelter, and clothing, while wants are desires like the latest gadgets or trendy fashion. Learning to prioritize needs over wants helps in making responsible spending decisions.

2. Spend Less Than What You Earn:

This classic financial principle is the cornerstone of sound money management. By consistently spending less than what you earn, you create a surplus that can be directed towards savings and investments, contributing to long-term financial stability.

3. Set Saving Goals:

Establishing clear saving goals provides a roadmap for financial success. Whether it’s saving for education, a car, or an emergency fund, having specific targets motivates disciplined saving habits.

4. Consider Investing at Your Earliest Opportunity:

Investing early can yield significant long-term benefits due to compound interest. Teenagers can explore low-risk investment options or consider investment platforms like Invstr Jr to dip their toes into the world of investing.

5. Build Skills That Can Help You Build Your Career:

Investing in skills is an investment in future earning potential. Building a strong skill set enhances career prospects, leading to increased income opportunities.

6. Learn About Debt:

Understanding the implications of debt is crucial. While some debt, like student loans, may be considered an investment in the future, high-interest consumer debt can lead to financial strain. Make informed decisions and manage debt responsibly.

7. Start Building Your Credit as Early as Possible:

Establishing a positive credit history early on is beneficial for future financial endeavors, such as obtaining a car loan or a mortgage. Responsible use of credit cards and timely payments contribute to a favorable credit score.

8. Focus on Building Multiple Streams of Income:

Diversifying income sources reduces financial vulnerability. This could involve part-time work, freelance gigs, or exploring entrepreneurial ventures.

9. Try to Avoid Peer Pressure:

Peer pressure can lead to impulsive spending. Developing the confidence to make independent financial decisions helps resist unnecessary expenditures influenced by peers.

10. Develop Great Saving Habits:

Cultivating a habit of saving consistently, even with small amounts, reinforces financial discipline. Automatic transfers to a savings account can make this process seamless.

11. Create a Budgeting Plan:

Budgeting is a roadmap for financial success. It involves allocating funds for various expenses, ensuring that spending aligns with financial goals.

12. Find Opportunities to Earn:

Actively seek opportunities to earn money, whether through part-time jobs, internships, or entrepreneurial ventures. This not only provides income but also valuable real-world experience.

13. Learn About Taxation:

Understanding basic tax principles is essential. Learn about different types of taxes, deductions, and credits to optimize financial planning.

By embracing these 13 top tips, teenagers can embark on a journey of financial literacy that will not only empower them in their formative years but also set the stage for a financially secure and prosperous future. Remember, financial literacy is not just about managing money; it’s about taking control of one’s financial destiny.

How can parents support their teenagers with learning about money?

Introducing teenagers to the intricacies of managing money is a crucial aspect of their overall education. Parents play a pivotal role in shaping their children’s financial values and habits. Here are several tips for parents to effectively support their teenagers in developing a strong foundation in financial literacy:

Leading by Example:

One of the most powerful ways parents can instill financial literacy in their teenagers is by leading through example. Demonstrating responsible financial behavior, such as budgeting, saving, and investing, creates a tangible model for teens to follow.

Open Communication about Money:

Fostering an environment of open communication about money is essential. Encourage teens to ask questions, express concerns, and share their financial goals. Discussing family finances transparently helps demystify the subject and promotes a healthy attitude towards money.

Supporting with Setting Up Saving or Investment Accounts:

Actively assist teenagers in setting up their first saving or investment accounts. Platforms like Invstr Jr can provide a hands-on introduction to investing. This practical experience lays the groundwork for understanding financial markets and the potential benefits of investing.

Helping with Budgeting:

Teaching teens how to create and stick to a budget is a valuable life skill. Work together to outline income, fixed expenses, and discretionary spending. This exercise not only imparts budgeting skills but also helps teens prioritize financial goals.

Helping with Finding a Part-Time Job:

Encourage teenagers to seek part-time employment during weekends or school breaks. Beyond the financial benefits, part-time jobs expose them to real-world work environments, instilling a strong work ethic and a sense of responsibility.

Setting Financial Goals:

Collaborate with your teenager to set realistic financial goals. Whether saving for a significant purchase, a college fund, or investing for the future, establishing clear objectives provides motivation and a sense of accomplishment as they make progress.

Credit Education:

Educate teenagers about the importance of responsible credit use. Discuss the basics of credit scores, the impact of timely payments, and the potential consequences of accumulating high-interest debt. Instilling credit awareness early can prevent financial pitfalls in the future.

Charitable Giving:

Introduce the concept of charitable giving to instill a sense of social responsibility. Encourage teens to allocate a portion of their income or allowances to charitable causes. This not only contributes to the community but also fosters empathy and a broader perspective on money’s role in society.

In conclusion, parents can significantly influence their teenagers’ financial literacy by adopting a proactive and supportive approach. By leading by example, fostering open communication, assisting with practical financial tasks, and imparting key financial concepts, parents lay the groundwork for a lifetime of responsible money management. The tips provided not only guide teenagers toward financial empowerment but also strengthen the parent-child bond through shared financial experiences. Ultimately, the goal is to equip teenagers with the skills and knowledge needed to navigate the complexities of the financial world with confidence and competence.

Great resources to help with teens learn about financial literacy

In the dynamic landscape of financial education for teenagers, Invstr Jr emerges as a comprehensive and innovative solution, offering a tailored approach to various aspects of financial literacy. Designed specifically for teens, Invstr Jr combines elements of a savings bank account, a budgeting resource sheet, and features for setting goals and allowances. Let’s delve into the unique features that make Invstr Jr a standout resource for teenage financial empowerment:

Invstr Jr’s Savings Account:

Invstr Jr functions as a savings account, providing a secure and user-friendly platform for teens to manage their money. Through this feature, teens can experience the fundamentals of saving, setting aside funds for specific goals, and monitoring their account balance.

Why it’s Great:

Invstr Jr’s savings account transforms the abstract concept of saving into a practical, hands-on experience. It enables teenagers to cultivate responsible saving habits in an environment that mirrors real-world financial scenarios.

Budgeting Resource Sheet:

The platform includes a budgeting resource sheet, offering teenagers a structured tool to manage their expenses. This feature allows teens to categorize their spending, allocate funds to specific areas, and gain insights into their financial habits.

Why it’s Great:

The budgeting resource sheet in Invstr Jr empowers teens with a tangible method to organize and understand their finances. By breaking down expenses into categories, teenagers can develop a clearer picture of their spending patterns and make informed decisions.

Invstr Jr’s Goals and Allowance Feature:

Setting financial goals is a crucial aspect of fostering responsible money management. Invstr Jr integrates a goals and allowance feature that enables teenagers to define specific financial objectives, allocate funds towards those goals, and track their progress over time.

Why it’s Great:

The Goals and allowance-setting features in Invstr Jr add a layer of gamification to financial education. By allowing teens to set and achieve goals, it instills a sense of accomplishment and motivation, making the learning process engaging and rewarding.

Comprehensive Financial Education:

Invstr Jr’s Holistic Financial Education Approach:

Invstr Jr doesn’t just stop at being a financial tool; it’s a holistic financial education platform. Through interactive modules, teens can explore a range of financial topics, including investing, understanding credit, and making informed financial decisions.

Why it’s Great:

Invstr Jr goes beyond the conventional boundaries of financial tools by providing a comprehensive educational experience. Teens not only manage their money but also gain a deep understanding of financial principles that will serve them well in the future.

In summary, Invstr Jr stands out as a multifaceted resource that goes the extra mile in nurturing financial literacy among teenagers. By seamlessly integrating features of a savings bank account, a budgeting resource sheet, and engaging tools for setting goals and allowances, Invstr Jr offers a unique and enriching experience. It is not just a platform for managing money; it is a dedicated space for teenagers to learn, practice, and thrive in the world of financial literacy.

Conclusion

The journey toward financial empowerment for teens involves a thoughtful combination of hands-on experience, practical tools, and comprehensive education. In this quest, several resources stand out, and none more so than the holistic solution tailored explicitly for teenagers – Invstr Jr.

The concept of financial literacy for teens extends far beyond the traditional piggy bank or basic lessons on saving money. It encompasses a dynamic set of skills ranging from investing and budgeting to understanding credit and making informed financial decisions. Invstr Jr encapsulates all these facets, offering teenagers a virtual haven where they can not only manage their money but also gain a profound understanding of the financial world.

Invstr Jr’s commitment to comprehensive financial education sets it apart. It goes beyond being a financial tool; it’s an educational platform where teenagers can explore various financial topics. Investing, understanding credit, and making informed decisions become integral parts of their financial arsenal.

In conclusion, as parents, guardians, and mentors, our responsibility is to equip the younger generation with the skills and knowledge they need to navigate the financial world successfully. Invstr Jr emerges as a beacon in this endeavor, offering a holistic approach to financial literacy for teenagers. It’s not just a platform; it’s a pathway to shaping financially empowered individuals who can confidently face the challenges and opportunities that money presents. As we encourage teenagers to explore the diverse facets of financial literacy, let Invstr Jr be the compass that guides them toward a future of financial independence and success.

All investing involves risk and can lead to losses.

Past performance does not guarantee future results.

Invstr Financial LLC (Invstr) is registered as an advisor with the SEC. Securities trading is offered to self-directed investors by Social Invstr LLC, a member of FINRA.

State-backed hackers from Russia, China, and Iran have been found to use Microsoft’s AI-based tools to improve their own malpractices.

Continue reading

The average American consumer cares about what has gotten cheaper or deflated.

Continue reading